Late-stage investment ROIs are often six times more than S&P 500 returns. What’s more, investing in late-stage companies is often viewed as “less risky” than supporting startups — but these ventures are still ventures. Here’s a look at risks that late-stage investors face and what this means for VC players.

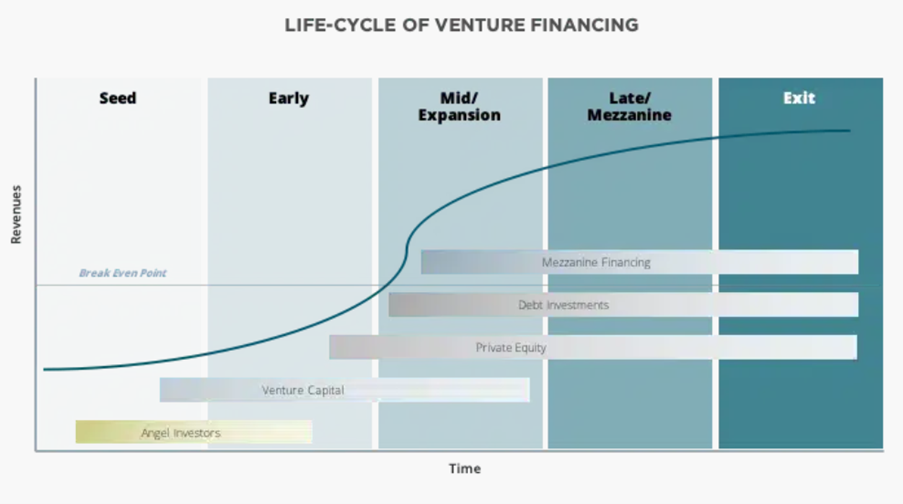

Venture Capital’s Life Cycle

From Seed funding rounds to an initial public offering (IPO), it’s helpful to know the life stages companies undergo. To begin, angel investors or friends and family frequently provide capital for startups to take flight. This Seed round is vital lifeblood at these beginning stages, averaging $500,000 to $2 million. As seen below, this round often serves as a stepping stone to bigger and better things, per se.

However, as a company grows and gains traction, founders launch more significant funding rounds. Typically, one investor leads, and other investors follow closely behind. Series A funding rounds, otherwise known as early venture financing, usually fall between $2 million and $15 million raised funds.

The scaling-up stage comes next, where founders often embark on a Series B round. Again, a primary investor typically leads this financing venture, and the funds average $7 million to $10 million. This venture financing is the mid-market or expansion stage.

As companies prepare to go public, owners use Series C to finish up final goals before an IPO. Even fewer companies embark on Series D or Series E, primarily for similar reasons as Series C. Known as late-stage or mezzanine venture financing, these rounds average $26 million.

Late-Stage Investment Risks

Businesses that are only six months to a year away from an exit, such as an IPO, are known as late-stage companies. Not only have these organizations proven their concept, but they’ve achieved significant revenues when stacked up against the competition. Here are a handful of late-stage company characteristics:

- They’re veterans of venture capital financing

- Annual revenue numbers are more than seven digits consistently

- They’ve outgrown their PEO and rely on an in-house HR system

- M&A suitors contend for their attention at this stage

High Return With Moderate Risk

Unlike startups in their infancy or some mid-market companies, late-stage companies aren’t as susceptible to quick collapse. Strangely enough, investors often create a frenzy trying to get on board with a pre-IPO company. Some say this is the fear of missing out (FOMO) syndrome.

The reason is that late-stage companies don’t possess the same level of risk as any other companies. Investors can enjoy many of the benefits, such as the risk premiums, that a private company offers while incurring a hefty return.

On that same note, most late-stage companies have already made their “mistakes,” leaving significant default risks in the dust of the past. However, even with increased predictability, there are risks late-stage investors face.

Cash Flow

Although late-stage companies are often cash flow positive, there’s still a risk of cash flow inconsistency. Take the COVID-19 pandemic, for example, and the devastation it caused all-sized companies. Aside from economic slumps, unusual market trends, or unexpected pandemics, late-stage companies still face annual revenue uncertainty.

Competitive Landscape

Competition is an aspect of business that not even late-stage companies can escape. That said, late-stage investors must endure the risk of other companies skyrocketing to the top regarding revenue and customer acquisition. In a worst-case scenario, an investor could lose a massive chunk or all of their investment.

Operating Cycles

Companies with short operating cycles can recover their inventory investment and on-hand cash quickly. Conversely, long operating cycles leave companies struggling to recover. Depending on which category a late-stage company falls, it might experience more vulnerabilities than another in the same stage.

Social Responsibility

Society is becoming more aware of the impact companies have on the environment. What’s more, many individuals have taken a stand against practices they deem harmful. These concerns are known as environmental, social, and governance (ESG) issues. For example, late-stage companies might leave a more significant carbon footprint or work with vendors with less-than-ideal practices, potentially creating a drop in valuation.

Respecting Risk Appetite

Not all VC investment firms are created equal — not all risks are created equal, either. Finding an investment firm to take on your particular risk level might not be as simple as dipping into your previous Series A or B network. Those particular investors might only feel comfortable in the early stage as opposed to late-stage investments. Additionally, most companies embarking on a Series C, D, or E typically depend on a highly exclusive investor circle.

Finding a good match is imperative. Late-stage investors must consider asset classes, age-based risk, and many other factors before deciding whether to invest. However, plenty of public market investors currently look for pre-IPO companies to establish their market position. And these same investors want liquidity as late-stage companies prepare to go public or an acquisition, and late stage company investment is a good bet.